I first wondered if the European Union (EU) and the Eurozone would survive in 2009, when Greece’s economy started to implode. The fear, back then, was that if Greece failed, it would be the domino that would lead to the collapse of the Euro and the EU. What made Greece so frightening was that it was the smallest of the PIIGS. (Portugal, Ireland, Italy, Greece and Spain).

Today, Greece is still in trouble. “Europe’s most indebted state is locked in talks with officials representing the European Stability Mechanism, the European Commission, the European Central Bank and the IMF over the terms attached to the loans keeping it afloat since 2010.” [1] The ongoing bailout and harsh austerity measures have devastated the lives and finances of many Greek citizens.

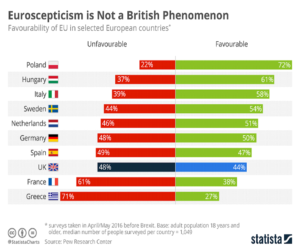

The big issue eight years ago was primarily economic. That is no longer the case. Islamic State inspired terror attacks in London, Berlin, Nice, Brussels and Paris have caused many Europeans to wonder if their governments can protect their citizens from terror attacks. These attacks have also strengthened the popularity of a growing number of right wing anti-immigrant parties.

Last June, BREXIT happened and Prime Minister Cameron resigned. Across Europe, right wing parties claimed that only they had a solution for the unprecedented rise in anti-EU sentiment.

In November, Donald Trump was elected President of the United States. During his campaign he questioned the continued relevance of NATO and the EU to America’s national interests.

A month later, Italian voters rejected constitutional reforms proposed by Prime Minister Renzi. This vote caused him to resign. It also strengthened the political power of the anti-establishment Five Star movement and the anti-immigrant Northern League.

On March 15, 2017, Geert Wilders, the anti-Muslim and anti-EU populist, lost his effort to become the Prime Minister of the Netherlands. While this was a victory for a pro-EU party, Wilders’ party gained five seats (+33%) to become the second largest party in the Dutch Parliament. Prime Minister Mark Rutte’s party lost 8 seats (-19.5%) and must form a coalition with four other parties before he can create a new government. If that happens, it will be the largest multi-party government that Holland has seen since the 1970s.[2]

In April, France will vote for a new President and at present, anti-EU crusader Marine Le Pen is the front runner. Most experts believe that she cannot win the April election outright and will not win a runoff in May. Finally, in late September, Germans will decide whether to retain the services of Chancellor Angela Merkel.

All across Europe, Europeans are questioning whether the EU should continue to exist in its current form.

A quarter of a century ago the EU and the Euro were viewed by many Europeans as the culmination of a decade’s long dream of European unification. So any conversation about the future of the EU must start with a discussion of why the EU was created in the first place.

When World War II ended, most of Europe had been devastated and more than seventy million people had been killed. Many Europeans believed that the only way to prevent another world war from starting in Europe was to link Europeans countries as closely together as possible. The first step was to foster economic cooperation. The idea being that countries that trade with one another become economically interdependent and so more likely to avoid conflict.[3] By the late 1960s, many believed that this effort was Europe’s best hope for stability and an environment of higher growth and employment.[4]

The European Economic Community (EEC), designed to increase economic cooperation between six countries – Belgium, Germany, France, Italy, Luxembourg and the Netherlands – was created in 1957. What began as a purely economic union evolved into an organization spanning policy areas, from climate, environment and health to external relations and security, justice and migration. A name change from the European Economic Community (EEC) to the European Union (EU) in 1993 reflected this expanded focus.[5] And, the six original members of the EEC added over time and in stages twenty-two additional countries.

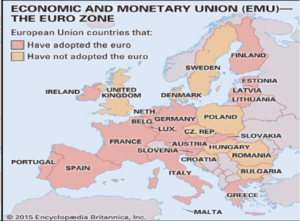

The Economic and Monetary Union (EMU) was launched in 1992. The EMU represented a major step to try to integrate the economies of EU members. The EMU is responsible for the coordination of economic and fiscal policies, a common monetary policy, and a common currency, the euro.

When the idea of the euro was first discussed, several economists warned against the creation of a common currency. They said that things might work out fine under a common currency as long as the overall European economy performed well. However, in case of an economic crisis, they warned, a common currency meant that member states would no longer be able to devalue their currencies. This is what most countries do to absorb the first shocks of an economic crisis. But you can’t do this if you have abandoned your national currency for the euro.

Some economists also believed that the creation of a common currency would hurt smaller countries with weaker economies more than larger countries with stronger economies. They feared that a common currency could cause resentment between nations in the Eurozone.

In spite of these warnings, the euro was launched on January 1, 1999 as a virtual currency for cash-less payments and accounting purposes. Banknotes and coins were introduced on January 1, 2002. While all 28 EU Member States are member of the economic union, some countries have taken integration further and adopted the euro. Together, these countries make up the euro area.[6]

The third piece of this unprecedented effort of European unification was the creation of the European Central Bank. The European Central Bank (ECB) is the central bank of the 19 European Union countries which have adopted the euro. Its main task is to maintain price stability in the euro area and so preserve the purchasing power of the single currency.[7]

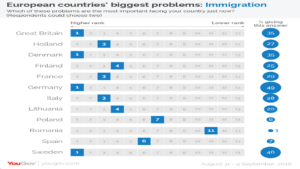

I have shared some of my thoughts about the political issues that bedevil the EU in my earlier piece – BREXIT, Trump and Ugly Baby Glasses.[8] Of all of the issues facing the EU, “immigration was given as the most important problem by the people of four countries: Britain, Denmark, Germany and Sweden. Of the 13 issues featured, it came in the top four issues for nine of the countries, with only Poland, Spain and Romania considering it to be a less important issue.”

As important as immigration is to the political debate about the EU’s future, I believe that the biggest challenge that the EU faces today starts and ends with the euro. The EU has twenty-eight members, but only nineteen gave up their national currencies to use the euro.

Layering the euro on top of the EU was never a good idea. For a currency to work, the issuing government must have the ability and the authority to use whatever fiscal and monetary policy tools its central bank feels are appropriate to address the specific challenges that its economy faces. When nineteen sovereign countries gave up their own currency to adopt the euro, they created the conditions for an economic disaster. In addition, “allowing” EU members to opt out of the euro meant that the European Central Bank did not have the power to “regulate” the EU’s economy.

When the EU said that it wanted to create “an environment of higher growth and employment,” it wasn’t being completely transparent. What EU really meant was the creation of euro and the European Central Bank were part of a process that many hoped would lead to a mechanism to transfer wealth from the EU’s strongest economies to its weakest economies.

There is nothing inherently wrong with a wealth transfer scheme if it is voluntary and all affected countries agree to do so. But for it to be positive, it must be part of a process to help the recipients develop stronger and more viable economies. But that is not what happened in Europe. Neither the EU nor the euro were designed to help Europe’s weak links learn how to become more competitive.

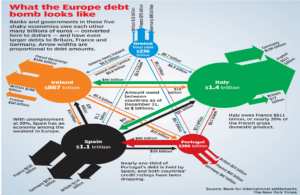

A basic economics concept explains the problem with the common currency in an extraordinarily simple way. Some countries entered the European Monetary Union with a higher rate of wage and price inflation than others to start with. The real interest rate (the nominal rate of interest less the expected rate of inflation) was therefore lower in high inflation countries like Spain than in others with low inflation countries like Germany.

If we compare the economies of Spain and Germany when the euro was created, the challenge the euro created becomes even clearer. This lower real interest rate, in addition to Spain’s relative size to German, French and UK economies, increased up demand in Spain and amplified wage and price inflation even more. Instead of being able to use different interest rates to bring inflation to the same level, Spain found her differences were aggravated by the single rate.

While the increase in demand for products produced by southern block of EU members seemed attractive at the beginning, the introduction of the euro spurred the creation of deficit spending. These deficits are at the center of the difficulties today.

This explains why Germany has become a large creditor while Spain has become substantial debtor.

Things were still working out reasonably well so long as the global economy was growing. But when growth stalled and the world was plunged into a global recession, it became clear that the euro and the ECB actually made things worse.

The global economic crisis of 2008 demonstrated the troubles associated with trying to partially unify the economies of independent, sovereign countries. Because the 19 euro zone members had given up their domestic currency, they lost the ability to implement fiscal and monetary policies most appropriate to the specific challenges that their local economies faced.

The European Central Bank is a blunt instrument that simply cannot address the country specific needs of Slovenia, Germany, Greece and Spain with one set of fiscal and monetary tools. But that is all that it had at its disposal.

George Soros was very perceptive when he said that:

“After the crash of 2008, a voluntary association of equals was transformed into a relationship between creditors and debtors, where the debtors had difficulties in meeting their obligations and the creditors set the conditions the debtors had to obey. That relationship has been neither voluntary nor equal.

After the Crash of 2008, the EU and the Eurobond became increasingly dysfunctional. Prevailing conditions became far removed from those prescribed by the Maastricht Treaty, but treaty change became progressively more difficult, and eventually impossible, because it couldn’t be ratified. The Eurobond became the victim of antiquated laws; much-needed reforms could be enacted only by finding loopholes in them. That is how institutions became increasingly complicated, and electorates became alienated.

The rise of anti-EU movements further impeded the functioning of institutions. And these forces of disintegration received a powerful boost in 2016, first from BREXIT, then from the election of Trump in the US, and on December 4 from Italian voters’ rejection, by a wide margin, of constitutional reforms.”[9]

This is what a Strategic Inflection Point looks like. If the Eurozone doesn’t recognize the severity of the challenges, it will die.

Today, we connect many of EU’s troubles, including the rise of nationalism, with the refugee crisis, with failing immigration policies or an inability to keep borders safe.

Ugly baby glasses require that we objectively evaluate data to see the way things really are before we inject our personal or political views into trying to understand what is happening. Otherwise, we humans have a tendency to play the confirmation bias game and see things the way we wish them to be. If you just focus on the data, my ugly baby glasses analytical tool will help you get to the root of the problem, identify the true concerns you face and take a politically agnostic approach to what fundamentally needs to change.

In this case, EU citizens need to look inside their own organization for deeper problems before they focus on concerns created primarily by outside factors, such as the Syrian refugee crisis.

So, can the EU be saved? Yes. Will it be saved? That depends on what its leaders do this year.

I believe that the number one thing that must be done to save the EU is for EU members with weak economies to leave the euro zone and reauthorize their national currencies. The common currency hurts their economies deeply. Helping them retire the euro is the best recommendation, as complex as it would be.

If EU members with weak economies make the decision to leave the euro, the transition will not be easy. The minute they announce that they are considering abandoning the euro, for example, they will experience a run on their banks. We have seen this movie before in Greece and Spain, just to give two examples. But the EU’s weakest economic members really don’t have a choice. Their banking systems are already staggering and unable to provide all the liquidity that their economies need to grow.

For those who are frightened by this idea, I remind you that that this has been the reality in weak European economies for almost a decade. Nothing suggests that things will get better for these countries if they stick with the euro.

The data is clear. This is what should be done. The only question is whether the leaders and members of the EU have the political will to make hard choices.

______________________________________________________________________

I am deeply indebted to one of my former Executive MBA students who has now become a trusted colleague for helping me with research on this article. We had many “energetic” conversations about the future of the EU and the Eurozone. We will continue to collaborate on this and other issues, leading to our producing a book in the future. Once she has received permission from her employer to be listed as a collaborator, her name will appear on those articles that she helps me produce.

[1]https://www.bloomberg.com/news/articles/2017-01-30/greek-markets-tumble-amid-bailout-review-deadlock-imf-concerns

[2] http://www.cnn.com/2017/03/21/europe/dutch-election-official-result/

[3]https://europa.eu/european-union/about-eu/eu-in-brief_en

[4]https://ec.europa.eu/info/about-european-union/euro/history-euro/history-euro_en

[5]https://europa.eu/european-union/about-eu/eu-in-brief_en

[7]https://www.ecb.europa.eu/ecb/html/index.en.html

[8]https://www.linkedin.com/pulse/brexit-trump-ugly-baby-glasses-john-n-doggett

[9]http://www.businessinsider.com/george-soros-essay-on-trump-defending-an-open-society-2017-1

Last modified: January 23, 2018